Quality Ideas at New Lows

Watching these 5 beaten-down companies

“The market is throwing us opportunities all of the time”.

Joel Greenblatt - author of The Little Book That Beats The Market - is right.

But let’s see more in detail if that’s the case for these 5 beaten-down companies.

In today’s brief:

5 potential defensive quality opportunities in today’s market

The surface Risk-Reward I’m seeing

Options ideas to monetize the wait

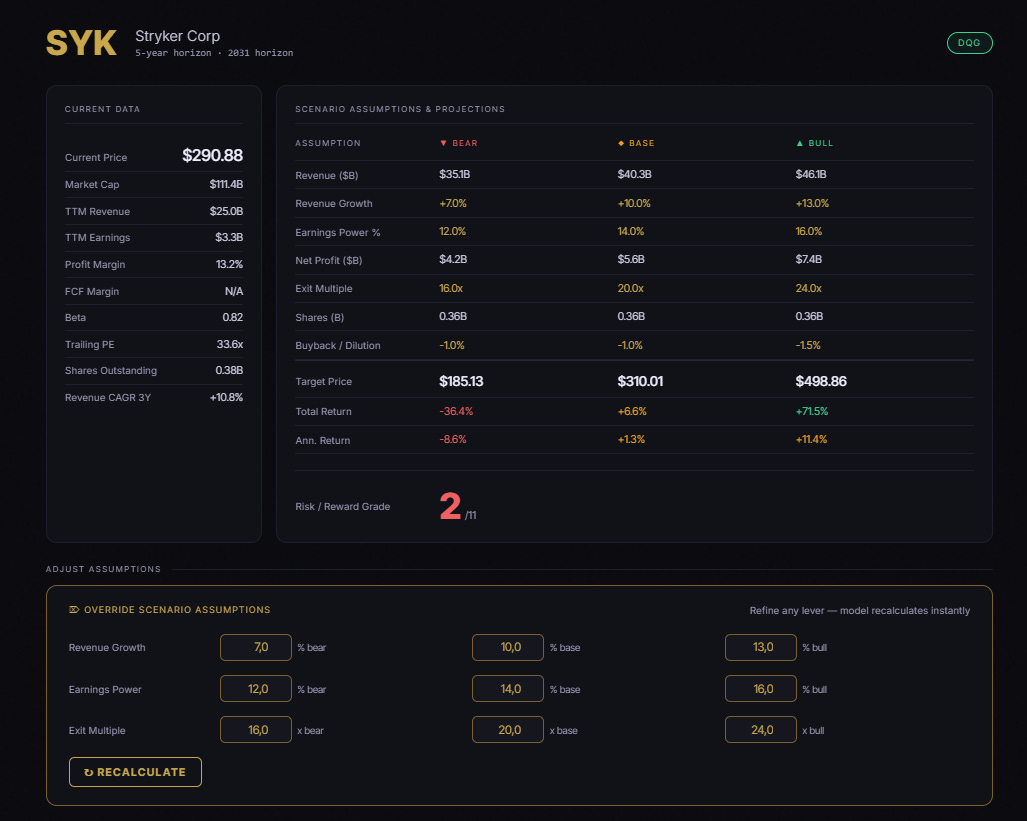

5. Stryker - SYK

📈 Stryker stock has delivered an unbelievable 15.5% CAGR since 1990!

Stryker is a healthcare company producing a variety of medical devices for surgical equipment, orthopaedics, spinal implants, neurovascular devices, and much more. In the investing world, it’s famous for being one of the historical holdings of UK legendary investor Terry Smith.

🎯 The surface risk-reward is showing a -36% downside and a +72% upside potential from current levels.

Based on educated assumptions I’ve done on revenue growth, marginality, and sentiment multiples.

➡️ Our correction sensitivity ladder is saying that the risk-reward would become favorable after a -25%, -30% correction:

Should SYK fall -25% amid unchanged original assumptions on revenue, earnings, and sentiment, the downside would be more protected and the upside more compelling, resulting into a risk-reward of 7 out of 11.

⬇️

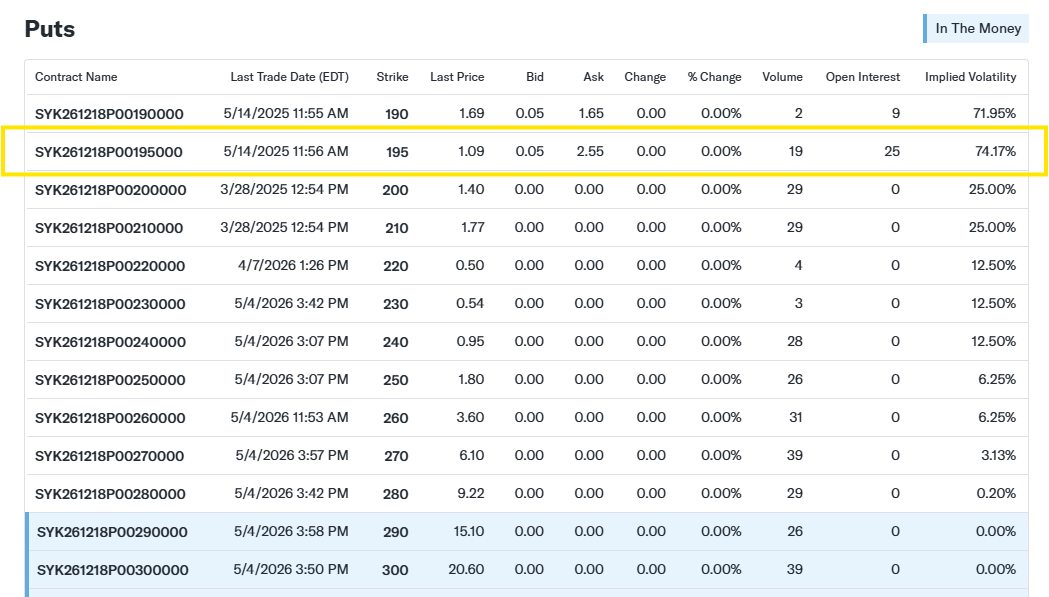

⌛ Can we monetize the wait with options?

I didn’t find interesting put options with a strike close to our target point of $185.

The only one is for Jun, 18 (45 days out), but I must say that:

implied volatility is high

bid-ask spread too wide

open interest (=volumes of contracts being exchanged) quite low

So for SYK, I’m passing on options for now.

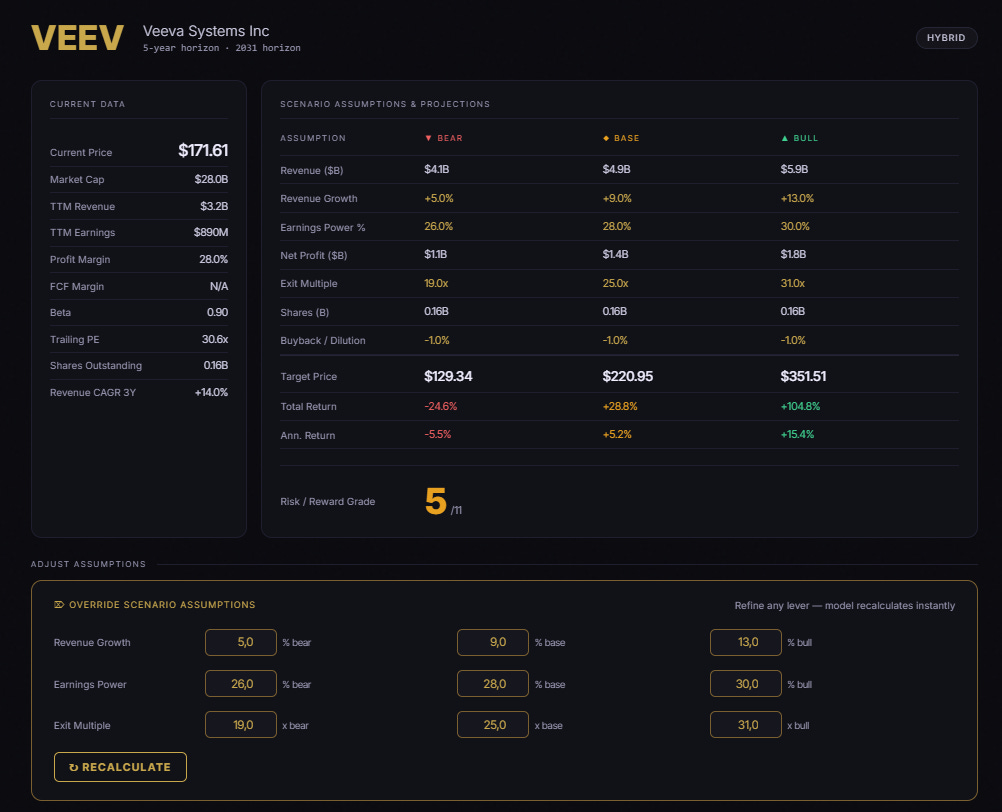

4. Veeva Systems - VEEV

📈 Veeva stock has delivered an unbelievable 12.9% CAGR since inception in 2014.

Basically flat over the past 6 years after the recent Saaspocalypse.

Veeva Systems is a software company that provides specialized software, data, and business consulting exclusively for the life sciences and pharmaceutical industries. They offer a variety of solutions, including clinical trial management, regulatory compliance, customer relationship management.

🎯 The surface risk-reward is showing a -25% downside and a +105% upside potential from current levels.

I’ve baked in several conservative projections such as revenue deceleration, margin compression, and weak sentiment.

➡️ Our correction sensitivity ladder is saying that the risk-reward would become favorable after a -10%, -15% correction:

Should SYK fall -15% amid unchanged original assumptions on revenue, earnings, and sentiment, the downside would be more protected and the upside more compelling, resulting into a risk-reward of 8 out of 11.

⬇️

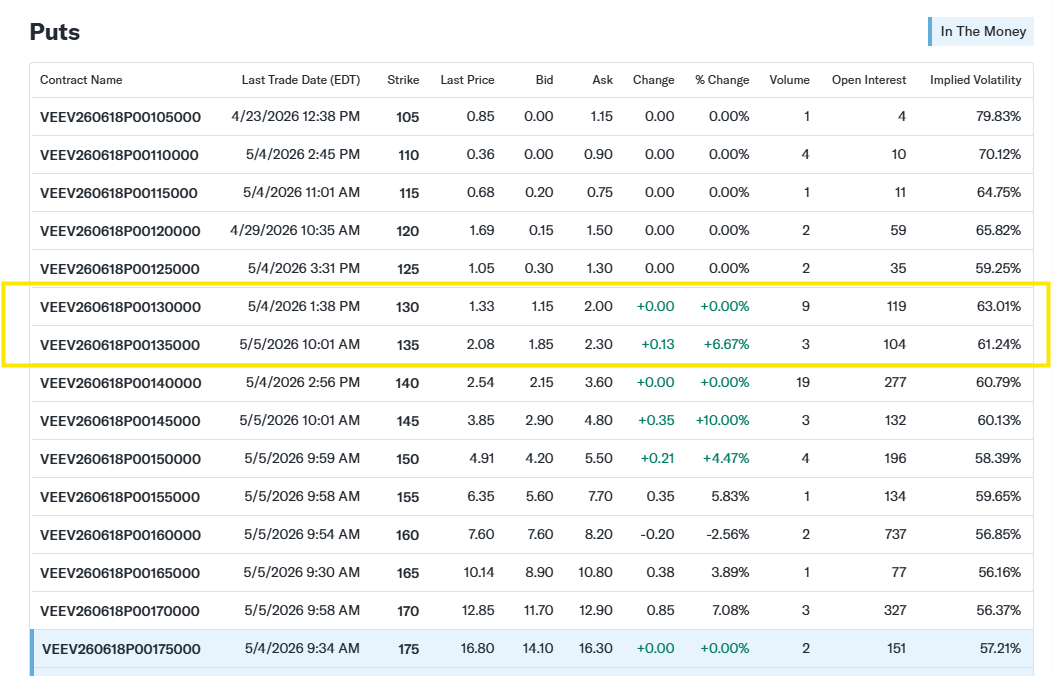

⌛ Can we monetize the wait with options?

Looking for deep in-the-money options at our bearish target price around $130, I found a put contract:

Strike: $135

Expiration date: June 18, 2026

Annualized return: +12.54% post broker fees as of last price of $2.08 premium per share

If you’re comfortable to hold Veeva at $135 anyways, and have the purchasing power to buy 100 shares without screwing up the position sizing of your portfolio, that’s an interesting opportunity.

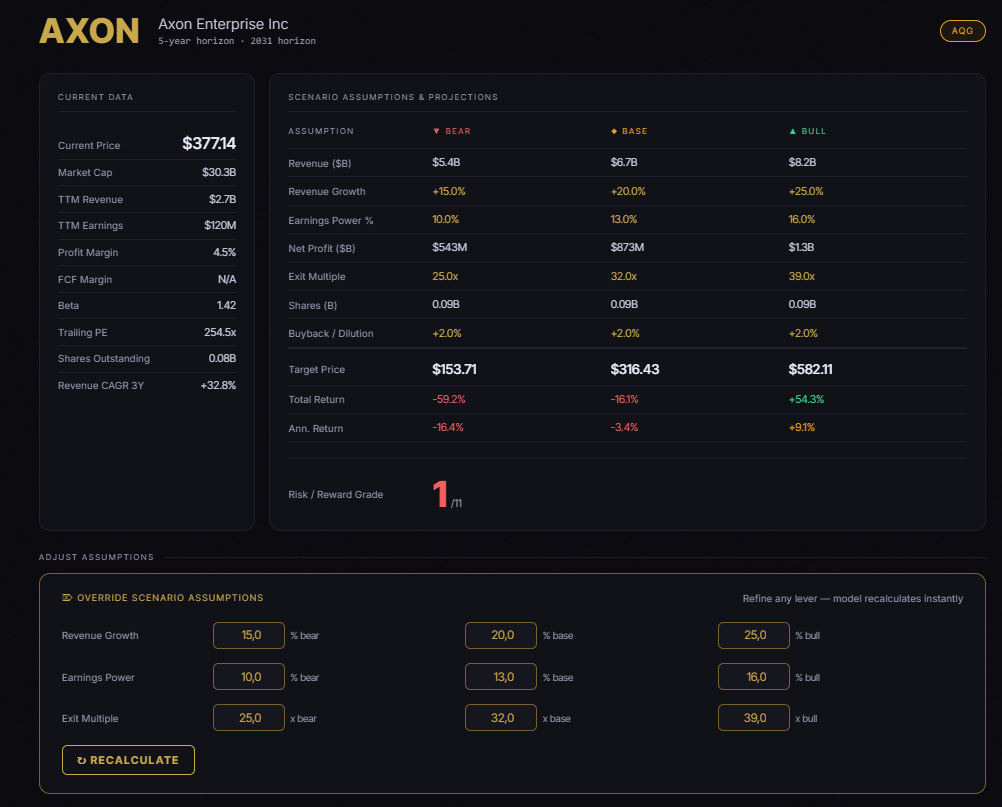

3. Axon Enterprise - AXON

📈 Axon stock has delivered an unbelievable +29.8% CAGR since 2022!

And this is despite of the recent -55% crash.

It doesn’t need introductions. Axon is perhaps the most popular safety technology company as they develop connected hardware and software solutions for the public safety. Best known as the manufacturer of TASER energy weapons and police body cameras, its integrated ecosystem is used by law enforcement, military, and private enterprise to improve their operations.

🎯 The surface risk-reward is showing a -59% downside and a +54% upside potential from current levels.

Despite some generous assumptions, I must honestly admit that this stock is still quite far from becoming appealing valuation-wise.

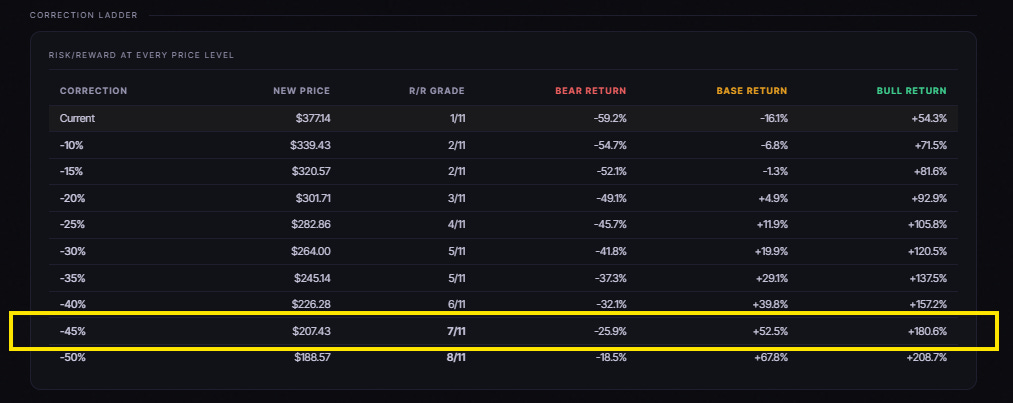

➡️ Our correction sensitivity ladder is saying that the risk-reward would become favorable after another -45% from here!

Should AXON stock fall -45% amid unchanged original assumptions on revenue, earnings, and sentiment, the downside would be more protected and the upside more compelling, resulting into a risk-reward of 7 out of 11.

⬇️

⌛ Can we monetize the wait with options?

My take here is no.

The strike price needs to be too much deep in-the-money, and I didn’t find anything at this stage.

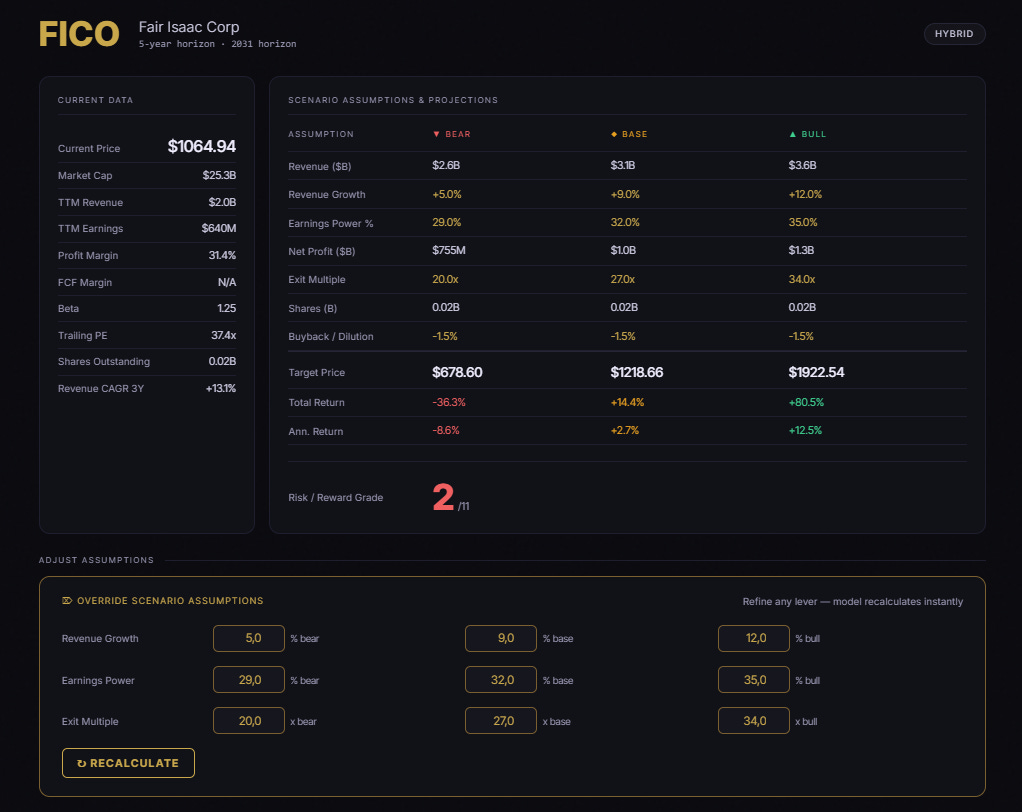

2. Fair Isaac Corporation - FICO

📈 FICO stock has delivered an unbelievable +21.1% CAGR since 1990.

That’s after the recent -56% crash (again).

FICO is the leader in data analytics company best known for developing the FICO Score, which is the standard measure of consumer credit risk in the United States. Beyond credit scoring, FICO also sells B2B software for fraud detection and consumer portfolio risk.

🎯 The surface risk-reward is showing a -36% downside and a +80% upside potential from current levels.

➡️ Our correction sensitivity ladder is saying that the risk-reward would become favorable after another -25% from here.

⬇️

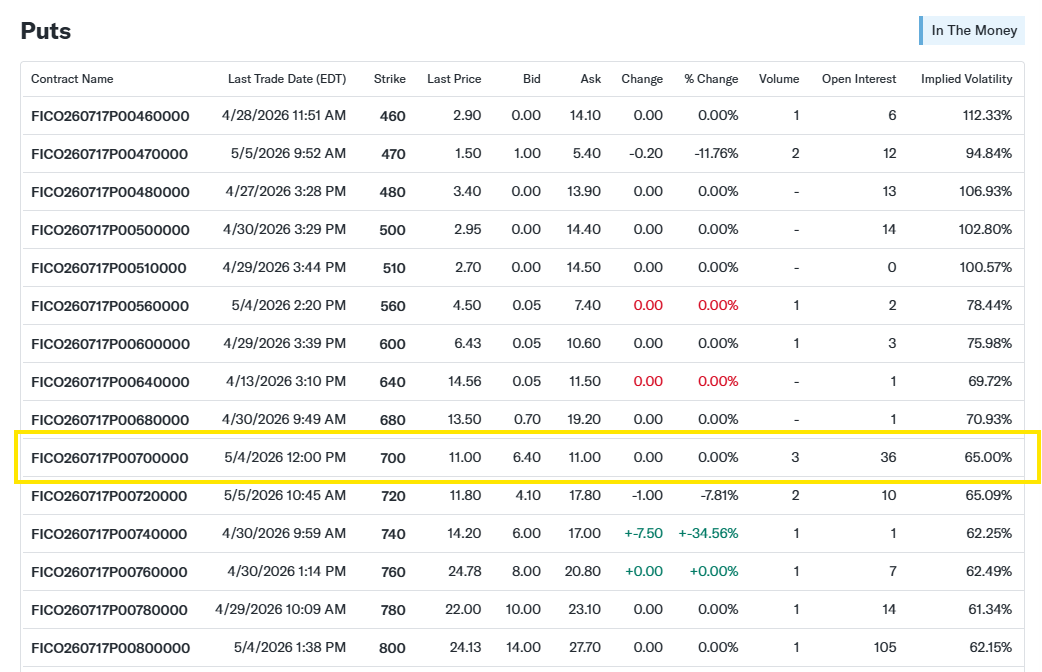

⌛ Can we monetize the wait with options?

Looking for deep in-the-money options at our bearish target price around $680, I found a put contract:

Strike: $700

Expiration date: July 17, 2026

Annualized return: +23.34% post broker fees as of last price of $6.40 premium per share (I assumed the worst pricing of the current bid-ask range).

If you’re comfortable to hold FICO at $700 anyways, and have the purchasing power to buy 100 shares without screwing up the position sizing of your portfolio, that’s an interesting opportunity.

This is for large portoflios only.

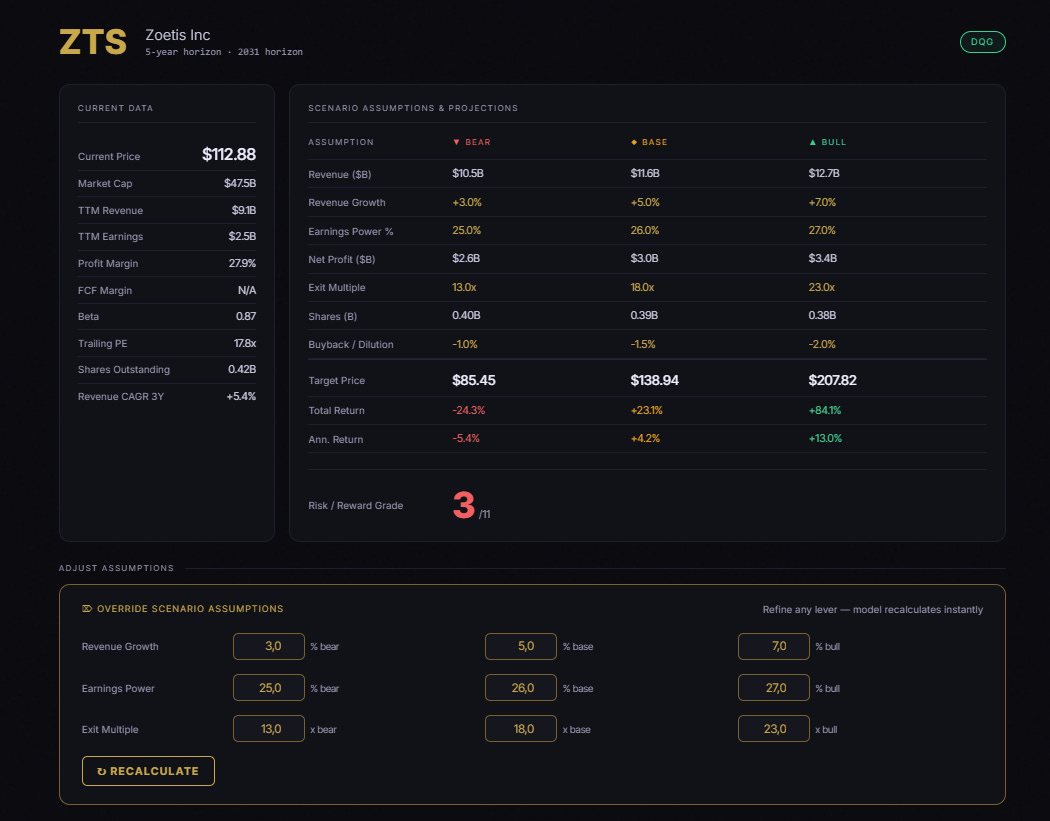

1. Zoetis - ZTS

📈 Zoetis stock has delivered a +10.3% CAGR since 2014.

That’s after the recent -54% crash.

Zoetis is the world’s leading animal health company. They discover, develop, manufacture, and commercialize a wide variety of veterinary medicines, vaccines, diagnostics, and digital technologies.

🎯 The surface risk-reward is showing a -24% downside and a +84% upside potential from current levels.

➡️ Our correction sensitivity ladder is saying that the risk-reward would become favorable after another -20% from here.

⬇️

⌛ Can we monetize the wait with options?

And once again my answer here is no.

I did not find interesting put option contracts:

around the $85 strike

with expiration date before the end of July

with enough transaction volumes

For options, I don’t look beyond the next couple of months, simply because I don’t want my option contract to be subject to future unknowns that may force me to change the underlying assumptions on the business.

Disclaimer & Rules of the Game

If you’re new, please consider the following rules on how to approach these analyses:

Target prices are always projected in a 3-fold scenario running on a 5-year basis.

They come as a result of the Top-Down Risk Reward Screener that I personally use for my research and inside the private AlphaZen program, whose assumptions have been defined on past stock research that may or may not need to be completed.

Being 5-year projections, stock prices can go way lower than that in the meantime.

This is not investment advice. Do your own research. I’ve been analyzing these companies for months, but my work may not be aligned to your specific needs.

I never buy or sell based on target prices only. There are many qualitative judgements to take into consideration before initiating a new equity position.

→ The goal of this analyses is not to provide answers, but to trigger the right questions moving forward with qualitative research.

Do these simulations on loop inside AlphaZen

If you find this content valuable and would like to implement rules-based investment decisions for yourself - I run a private program: AlphaZen.

You’ll grab the entire stack (video training, simulators, agents) me and my students are using to quietly compound our investments with peace and confidence.

You will also follow all my moves in real time and know what stocks I’m prioritizing above everything else, at what prices (they’re not the ones of today’s article).

Thank you again for your time.

📈

Happy Investing,

Francesco

Great write up! I like your various scenarios