Monetizing The Wait on 5 Ideas

Collect income by selling puts at our desired bear target prices

Dividends? No thanks.

It’s always been clear to me: my early retirement will be led by options.

The Main Idea (and Math behind it)

Let me be clear: at 33, I still have a few compounding cycles to pursue with my current wealth accumulation strategy before I switch to options and optimize my portfolio for income generation.

My goal for now is to learn, test, and journal so that I’m on point when the moment comes.

The cool thing about options - if used intelligently and in conjunction with our usual Value Investing principles - is that the underlying capital required to unlock career optionalities is much lower.

The reason is simple: if a semi-passive dividend strategy can generate 3%-6% per year, a basic options strategy like the ‘Wheel Strategy’ can generate between 0.6% and 1.2% per month, meaning 7% to 15% per year.

Let’s run some basic math.

If your lifestyle is, say, $50,000 per year (modest), how much underlying capital would you need to fund it without any other income source?

With dividends → between $833,000 and $1,667,000 (assuming 3%-6% yields per year)

With options → between $333,000 and $715,000 (assuming 7%-15% yields per year)

With options, you can decrease the steady-state portfolio size by 2.5x compared to what’s needed with dividends as income engine.

Not to mention treasury yields or the famous 4% withdrawal rule.

If your lifestyle is $100,000 instead, this is how much you’d need to generate it:

With dividends → between $1,667,000 and $3,330,000

With options → between $667,000 and $1,430,000

The options figures look undeniably way less ambitious compared to the starting point dividends would force you to achieve.

For my specific case, assuming my 27.8% annual returns from my regular value investing gets a sharp hair cut, opting for options as an income source would unlock a $50,000 lifestyle early retirement 7-8 years before any dividend income strategy could possibly do.

Meaning I could already activate the new strategy at the age 38-39 instead of waiting until the age of 46-47.

With that being said, it’s very unlikey that I will interrupt my regular part-time compounding strategy at 38. I will likely keep pursuing it further and let my AUM go for another 2x.

At that point, I could decide to stop around the age of 43-44 to fund a $100K/year lifestyle with options, or wait until 50-51 and let dividends take care of it. Of course, the first one would be my option, literally.

Does it make sense? I hope this feels relatable.

Now let me tell you more on what I’m doing now in 2026 with options, with a few concrete examples.

The Options Chain is just the last piece

The choice of the option is literally the last, obvious step of the underlying stock evaluation process.

In the past I also used to associate options to complex trading set-ups, but in reality it’s simple for us value investors.

If you’re happy to buy Amazon at $200, you can either do nothing or sell a $200 strike put on the open market expiring in 30 or 60 days, collecting a premium while you wait.

After the 30-60 days:

Amazon stock is above $200, and you keep the premium

Amazon stock is below $200 and you’re forced to buy it at a lower price ($185?)

But guess what, you were ready to own it at $200 anyways, and your break-even is now a bit below that, thanks to the premium.

I don’t want to simplify things too much, but the hard part here is not selling the option, but it’s rather establishing that $200 is an excellent risk-reward entry point for Amazon.

Which is exactly what my regular investing system is already about.

Thanks to my regular archives and watchlists, with clear asymmetric risk-reward indications, I already have dozens of potential monetized options ideas sitting there.

In the past 12-18 months or so, I’ve been running experiments with options on a separate, smaller portfolio and my goal is to kick-off a new, bigger one (maybe even public), starting 2027.

In the meantime, I’ve actually built a new options agent that I use in conjunction to my fundamental risk-reward screener to monitor interesting wheel strategy set-ups.

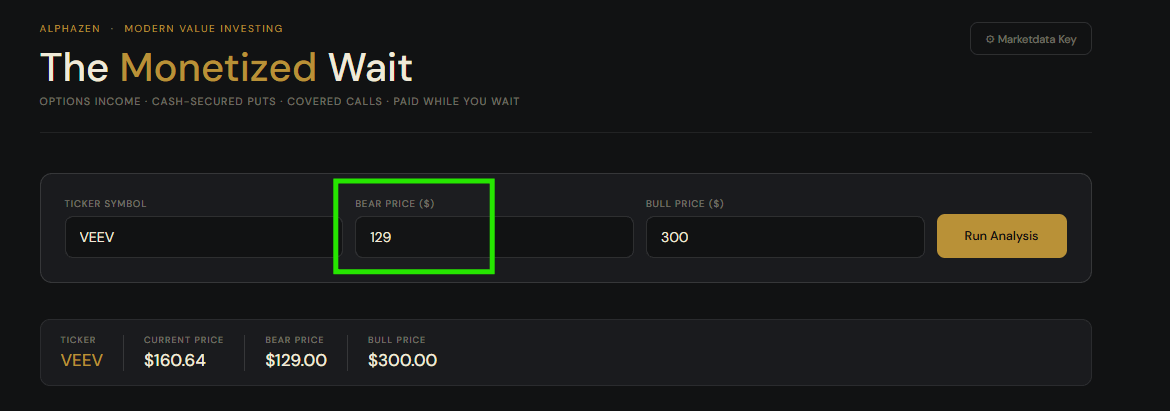

I called it The Monetized Wait™.

Let’s see 5 put options examples.

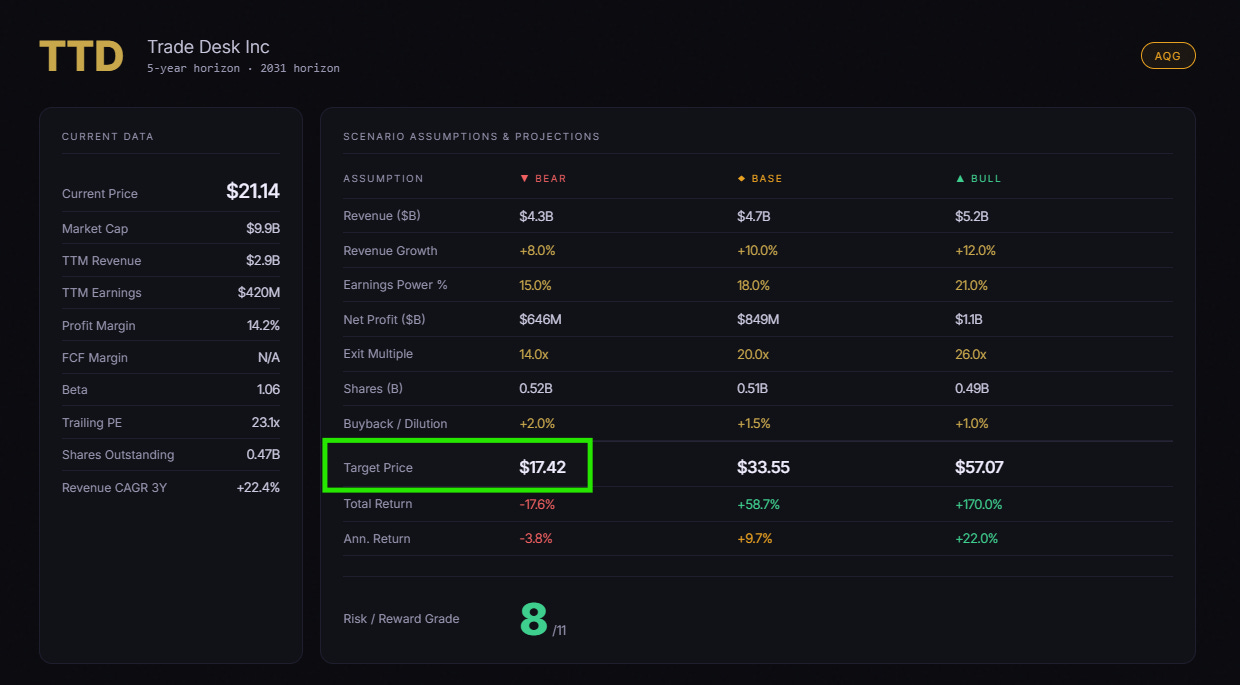

5. The Trade Desk

I won’t delve into all the underlying details on why I consider TTD asymmetric right now, but looking at the current risk-reward set-up:

I have a bear target scenario of $17.5 roughly.

So I then activated The Monetized Wait™ to see if there’s an interesting put option contract somewhere near $17.

A price I’d be happy to own TTD anyways 30 days from now.

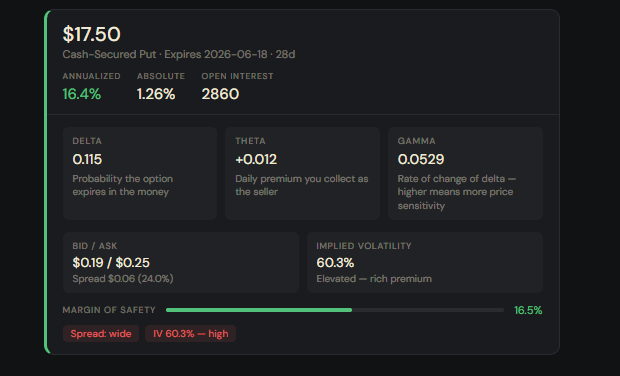

Result, there’s a $17.50 put option:

Expiring on June 18, in 28 days

With a delta of 0.115 → there’s 11.5% chances that the share price of TTD will fall below $17.50

With a +1.26% absolute return in 28 days → a+16.4% annualized

Not too bad.

So the process is simple:

I’ve extensively analyzed TTD stock with all my usual tools: valuation, risk management, risk-reward projections…

Concluded that the current risk-reward is attractive

Identified $17.50 as protected entry point

Found the option contract with the agent

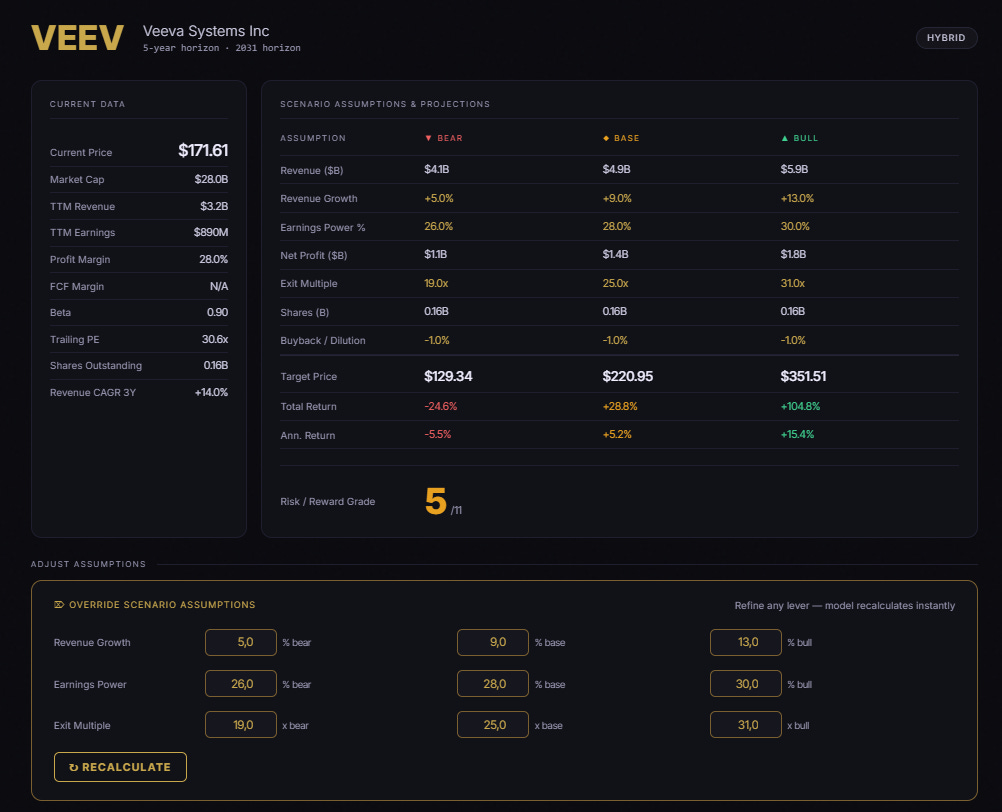

4. Veeva Systems

I told you about this company 2 weeks ago.

The Risk-Reward was a 5/11:

We could just pause it and forget about it, or…

Exploring options contracts with the Monetized Wait™ - setting $129 as ideal option strike price.

The agent will return options combinations around that strike price, with a return of at least 5% annualized, clearing out all options contracts that don’t exhibit low volumes, big bid-ask spread, or other weird characteristics.

For VEEV, I found:

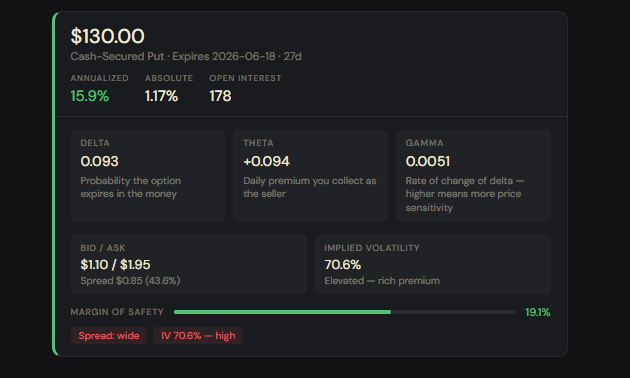

$130 strike price

27 days expiration

9.3% chances of “getting assigned” (check the 0.093 Delta)

+1.17% return in 27 days, +15.9% annualized

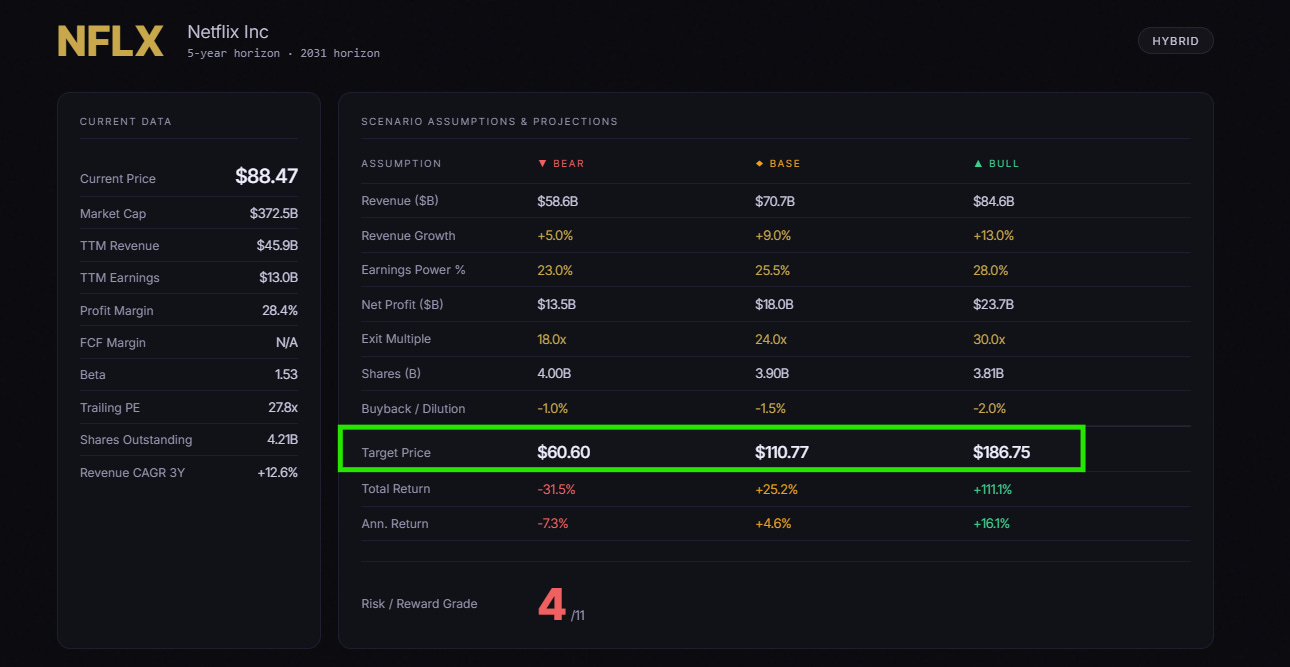

3. Netflix

Let’s do it again quickly for Netflix.

Let’s say you like it at $60, just like me:

Because it’s where the risk-reward would turn asymmetric in our favor.

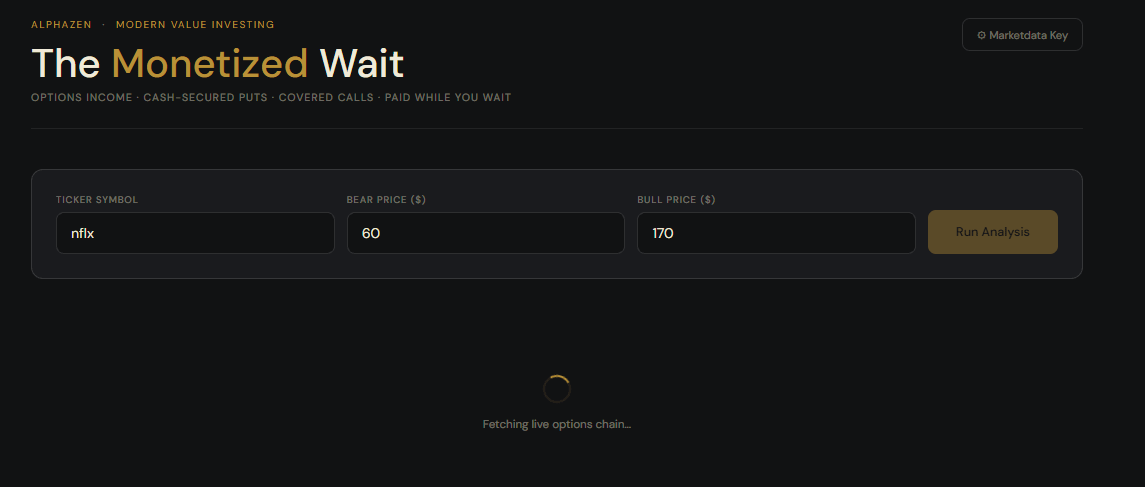

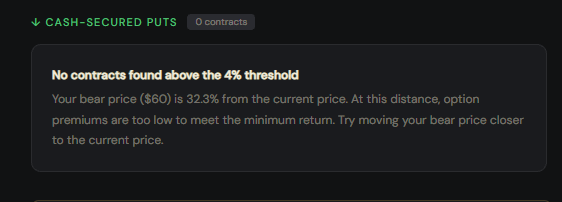

From there it’s just one click inside our Options Agent:

This time, the agent did not find interesting results.

It means that either the available options are too low in volumes (with very high bid-ask spreads) or that they don’t exist.

2. Uber

Uber is surprisingly showing an attractive risk-reward amid conservative assumptions on revenue growth, earnings power, and exit multiples… today.

Disclaimer: I don’t own shares and I’m not planning to.

Considering the relatively close bear target price of $66, I’m expecting to see interesting put option contracts.

Let’s discover it live, together:

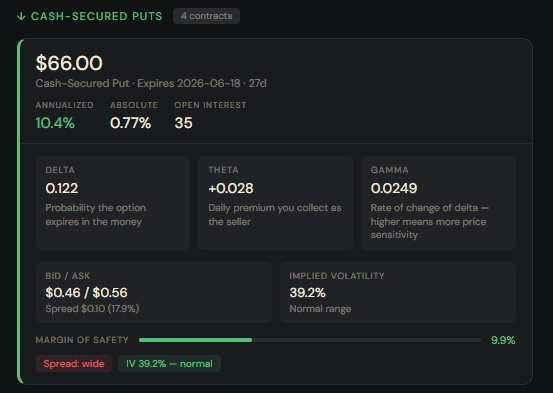

And here we go:

$66 strike

27 days expiration

+10.4% annualized return

12.2% chances of being forced to buy UBER at $66

That’s fun, isn’t it?

Last one before I ask for your opinion.

1. ServiceNow

I’ve dealt with NOW a lot lately.

Let’s close the loop today.

Backing in conservative assumptions on revenue growth and exit multiples, I’ve found $70 per share as the most cautious asymmetric entry point.

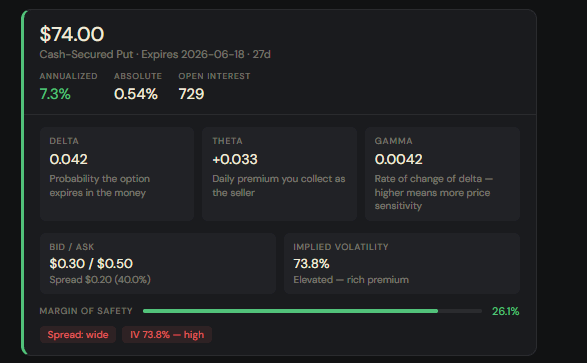

In terms of put options, you could make a +7.3% annualized return by selling a cash-secured contract with strike $74, expiring in 27 days, with a 4.2% chance of getting assigned.

Your Opinion Matters!

My entire investing stack will save you ages: grab it now!

For May only, I opened a special window lasting until May 31st to grab my entire system.

Everything that’s generating +27.8% per year in the past 5.5.

With a 8.5 reward-to-risk portfolio set-up going into the second half of 2026 (the best set-up in a while).

You’ll get:

all my training curriculum (20+ hours)

all my simulators

my portfolio and my watchlists

all my agents

a 1:1 Q&A with me at the end

It pays for itself on day 1.

Thank you again for your time.

📈

Happy Investing,

Francesco